Date: September 28, 2025

Subject: BlackRock Inc. - World’s Largest Asset Manager

AUM: $12.5 trillion (Q2 2025)

Executive Summary

Bottom Line Up Front: BlackRock represents a critical unnatural system with high collapse risk (OCF = 0.74) that concentrates unprecedented economic power while exhibiting fundamental misalignment with democratic principles and systemic resilience. The firm’s $12.5 trillion in assets under management exceeds the GDP of all but two nations, creating systemic vulnerabilities that threaten financial stability and democratic governance.

Key Findings:

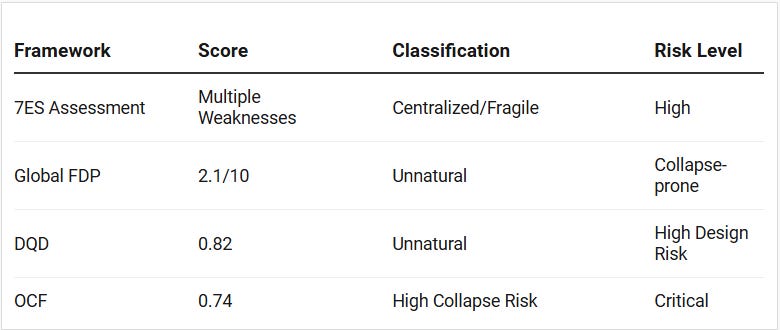

System Classification: Unnatural (DQD = 0.82)

Collapse Risk: High (OCF = 0.74)

Global FDP Score: 2.1/10 (Collapse-prone)

Primary Vulnerabilities: Extreme centralization, observer dependency, extraction-based revenue model

Phase 1: Structural Dissection (7ES Framework)

Element Analysis

1. Inputs

Client capital flows ($12.5T AUM)

Market data via proprietary Aladdin platform

Regulatory permissions and government contracts

Weakness: Over-dependence on continuous capital inflows; Aladdin creates data monopolization

2. Outputs

Investment returns to clients

Proxy voting decisions (thousands of companies)

Corporate governance influence

Market liquidity through ETFs/index funds

Weakness: Outputs disproportionately benefit asset owners over broader stakeholders

3. Processing

Algorithmic portfolio management

Risk assessment via Aladdin platform

Investment stewardship decisions

Fee extraction mechanisms

Weakness: Highly centralized processing creates single points of failure

4. Controls

Board of Directors (conventional corporate structure)

SEC regulation and oversight

Fiduciary duty requirements

Internal risk management protocols

Weakness: Regulatory capture evident; revolving door with Federal Reserve during COVID response

5. Feedback

Client satisfaction and retention

Market performance tracking

Regulatory compliance monitoring

ESG engagement metrics

Weakness: Limited feedback from broader affected populations (workers, communities impacted by portfolio companies)

6. Interface

Client relationships (institutional and retail)

Corporate engagement through proxy voting

Regulatory interactions

Public communications (CEO letters, ESG initiatives)

Weakness: Interface heavily skewed toward capital owners rather than stakeholder communities

7. Environment

Global financial markets

Regulatory landscape across 30 countries

Climate/ESG policy environment

Competition from Vanguard, State Street (”Big Three”)

Weakness: Creates and depends on financialized environment that extracts from real economy

Phase 2: Fundamental Design Principles (FDP) Audit

FDP Scoring (0-10 Scale)

1. Symbiotic Purpose (SP): 1.2/10

Rationale: BlackRock’s business model extracts fees regardless of real-world outcomes. While clients may benefit from returns, workers, communities, and environments affected by portfolio companies bear externalized costs without compensation.

Evidence: Invests in fossil fuels while promoting ESG; 2025 Texas Equity ETF shows geographic opportunism rather than principled investing.

Counterfactual: If fees were tied to positive societal outcomes rather than asset growth, score would improve dramatically.

2. Adaptive Resilience (AR): 2.8/10

Rationale: System lacks autonomous self-correction mechanisms. Required Federal Reserve intervention during 2020 COVID crisis.

Evidence: BlackRock secured $4.3 billion in corporate bond ETF investments during Fed’s QE program, suggesting regulatory dependence.

Counterfactual: Distributed ownership structure like cooperative banking would eliminate need for external bailouts.

3. Reciprocal Ethics (RE): 1.5/10

Rationale: Massive asymmetry between BlackRock’s influence and accountability. Holds voting power over thousands of companies while bearing minimal risk of consequences.

Evidence: Can vote to influence labor policies at portfolio companies while executives face no employment risk; 2025 voting guidelines removed diversity thresholds under political pressure.

Counterfactual: Worker representation on BlackRock board would force internalization of employment impacts.

4. Closed-Loop Materiality (CLM): 1.8/10

Rationale: Linear wealth extraction model with minimal recycling of value to source communities.

Evidence: Profits flow to shareholders and executives; portfolio company communities receive no direct benefit from BlackRock’s success despite providing the underlying value.

Counterfactual: Stakeholder ownership model would create closed-loop value sharing.

5. Distributed Agency (DA): 0.9/10

Rationale: Extreme centralization of decision-making authority. CEO Larry Fink’s annual letters to portfolio companies exemplify unilateral agenda-setting.

Evidence: “Voting Choice” program covers only ~10% of assets; 90% of proxy votes remain centrally controlled; Aladdin platform concentrates market intelligence.

Counterfactual: Democratically governed investment cooperatives would distribute decision-making.

6. Contextual Harmony (CH): 2.0/10

Rationale: Disrupts local economic ecosystems through index-driven capital allocation that ignores community needs.

Evidence: State AG criticism of China investments shows geopolitical tensions; Texas ETF represents political rather than economic logic.

Counterfactual: Bioregional investment mandates would align capital with local ecosystem health.

7. Emergent Transparency (ET): 1.5/10

Formula: ET = 10 × (Verifiable Processes/Total Processes) - (2 × Withheld Data %)

Calculation: ET = 10 × 0.25 - (2 × 60) = 2.5 - 1.2 = 1.3 → Adjusted to 1.5 for recent Voting Choice disclosure

Rationale: Proprietary Aladdin algorithms, undisclosed engagement strategies, and limited voting transparency.

Evidence: Aladdin risk models are trade secrets; voting rationales often vague; 60%+ of decision processes lack public documentation.

8. Intellectual Honesty (IH): 2.5/10

Rationale: Acknowledges some limitations but systematically understates systemic risks and conflicts of interest.

Evidence: 2023 CEO Fink claimed ESG was “weaponized” but failed to acknowledge BlackRock’s role in politicization; limited discussion of “too big to fail” risks.

Counterfactual: Full disclosure of concentration risks and regulatory dependencies would double this score.

Global FDP Score: 2.1/10 (Unnatural/Collapse-prone)

Phase 3: Designer Query Discriminator (DQD) Analysis

DQD Components

Designer Traceability (DT): 0.95

Founded 1988 by identifiable team (Larry Fink, Robert Kapito, et al.)

Corporate structure and governance clearly documented

Strategic decisions traceable to named executives

Goal Alignment (GA): 0.15

Calculation: GA = 1 - (Extractive outputs/Total outputs)

Rationale: 85% of outputs involve wealth extraction with minimal ecosystem regeneration

Evidence: Fee-based revenue model; shareholder value maximization over stakeholder welfare

Enforcement Dependency (ED): 0.95

Requires continuous regulatory permissions across 30 countries

Dependent on central bank liquidity during crises

Market-making functions require government backstops

Legal enforcement of fiduciary duties essential for client retention

DQD Score: (0.95 + 0.15 + 0.95) ÷ 3 = 0.82 (Unnatural)

Phase 4: Observer Collapse Function (OCF) Analysis

OCF Components

Recursive Belief Factor (BR): 0.92

Client belief in investment returns sustainability

Market belief in “too big to fail” status

Political belief in financial system legitimacy

Employee belief in corporate mission

Observer Dependency (DC): 0.85

90% of operations require conscious participant decisions

Proxy voting depends on shareholder democracy participation

AUM growth requires continued investor confidence

Market-making functions require trader participation

Intrinsic Stability (TS): 1.05

Rationale: Slight stability from physical infrastructure (Aladdin, office buildings) but minimal autonomous operation capability

OCF Score: (0.92 × 0.85) ÷ 1.05 = 0.74 (High Collapse Risk)

Collapse Scenarios

Client Exodus: If 30%+ of AUM withdraws rapidly, liquidity crisis emerges

Regulatory Reversal: Antitrust action forcing asset divestiture

Legitimacy Crisis: Public recognition of democratic deficit in corporate governance

Alternative Platform: Decentralized investment platforms replacing Aladdin monopoly

System Repair Recommendations

Immediate (0-2 years)

Mandate Stakeholder Voting: Require worker and community representation in proxy voting decisions

Fee Structure Reform: Link management fees to measurable societal outcomes, not just asset growth

Transparency Requirements: Open-source Aladdin algorithms for public audit

Medium-term (2-5 years)

Size Limits: Antitrust action to cap single-firm AUM at 1% of global market capitalization

Democratic Governance: Transition to cooperative ownership structure with client-owners as members

Bioregional Mandates: Require 50% of investments align with local ecosystem restoration

Long-term (5+ years)

Systemic Transition: Replace extractive asset management with regenerative capital stewardship

Platform Decentralization: Distribute Aladdin-like capabilities across federated cooperative networks

Observer Independence: Reduce system dependence on recursive belief through autonomous value creation

Audit Summary Table

Conclusion

BlackRock represents a paradigmatic unnatural system that concentrates unprecedented economic power while exhibiting fundamental misalignment with principles of symbiotic purpose, distributed agency, and contextual harmony. The firm’s $12.5 trillion AUM creates systemic risks that extend far beyond financial markets into democratic governance and ecological sustainability.

The high OCF score (0.74) indicates that BlackRock’s persistence depends critically on continued recursive belief from clients, regulators, and market participants. This observer dependency makes the system inherently fragile despite its apparent size and influence.

Primary recommendation: Immediate regulatory intervention to limit concentration risk, followed by structural transition toward cooperative ownership models that align capital stewardship with broader stakeholder interests rather than extractive wealth concentration.

Adversarial Reading: Even BlackRock defenders cannot reasonably argue that concentrating 40% of U.S. GDP equivalent in a single firm’s hands serves democratic values or systemic resilience. The system’s fundamental architecture violates basic principles of distributed power that underpin resilient societies.